The latest 2Q2022 findings of the Container Shipping Market Quarterly Review produced by MDS Transmodal and Global Shippers Forum (GSF), noted that average earnings per container carried had fallen for the first time since 2020.

Total container carryings in the second quarter of 2022 also remained lower than the year-ago level in the same period.

The report noted a small improvement in the reliability and consistency of port calls in the second quarter. However, suggests it was accomplished at the expense of skipping intermediate port calls.

The data reveals a high level of capacity lost to ‘skipped’ ports.

There are indications that container shipping service patterns are being reshaped.

In 2Q2022, there has been an increase in the number of services connecting no more than two regions, together with a reduction in those linking more than two regions.

This means long, multi-port ‘loop’ schedules are being replaced by ‘shuttle’ services with transhipments required at hub ports in order for containers to reach their ultimate destinations

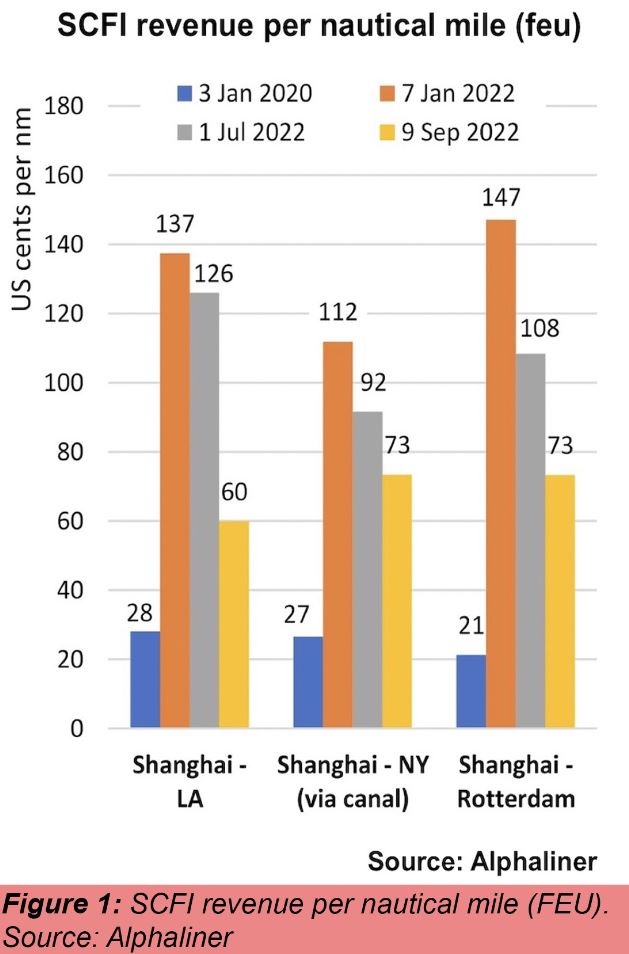

Spot ocean earnings have been sliding since the Shanghai Containerized Freight Index (SCFI) reached a high in January this year and ocean carriers are redeploying ships to more profitable trade lanes.

According to Alphaliner, the calculated revenues per nautical mile (nm) on the main East-West trade lanes revealed the Trans-Atlantic as the most lucrative trade, significantly outpacing the Trans-Pacific.

“Shifting extra tonnage to the North Europe – USEC trade can therefore be very rewarding,” Alphaliner noted.

Spot freight rates from Shanghai to California fell below USD 3,500 per FEU last week. Revenue per nm on this route has been halved since July and is down to 60 cents.

For both the Shanghai to New York and Shanghai to Rotterdam routes, revenues are now at 73 cents per nm. On the Trans-Atlantic from Rotterdam to New York, the figure stands at 217.9 cents per nm.

Plunging spot rates on the Trans-Pacific is a “major concern” for newcomers and non-alliance carriers.

While the average revenue on the Trans-Pacific is still more than double compared to pre-pandemic levels, newcomers and non-alliance carriers have fixed very expensive tonnage on the charter market and are typically very dependent on the spot market.

A Linerlytica report noted, “Several of the new entrants to the Asia-Europe and Trans-Pacific markets have significant tonnage commitments that will not allow them to easily remove their vessels in the short term.”

Alphaliner has suggested the industry will experience a widening two-tier market differentiated by those carriers who have signed long-term contracts at elevated rates, and those relying on the softening spot market.

New analysis released this week by BIMCO forecasts headhaul and regional volume growth dropping 1-2% in 2022 with 3-4% growth in 2023 as best case.

“The fleet supply/demand balance is predicted to worsen, and although carriers can maintain a tight cargo supply/demand balance by adjusting deployment, we predict that freight rates will continue to fall.

At the very least, contract rates must be expected to again move below spot rates,” the BIMCO container analysis reported.

Source: splash247.com